CBA bubble: passive vs active debate

- JASON TEH, Chief Investment Officer

- Jul 10, 2025

- 4 min read

Commonwealth Bank of Australia (CBA) is in the midst of a valuation bubble, defying the principle that long term stock returns are driven by earnings growth. Over the past three years, CBA’s share price has more than doubled, yet its earnings have grown at a modest 4% per year. In contrast, previous three-year periods of strong performance – such as 2005–2007 (15% annual earnings growth), 2010–2012 (17%), and 2012–2015 (8%) – were underpinned by significantly higher earnings growth.

Today, CBA’s rally is fuelled by an extraordinary expansion of its price-to-earnings (PE) multiple, which has reached unprecedented levels. As a result, CBA now represents approximately 10% of Australia’s total stock market capitalization.

If earnings growth isn’t driving this surge, a lower discount rate – through a lower risk-free rate or risk premium – might justify the higher PE ratio. However, Australian 10-year government bond yields, a proxy for the risk-free rate, has risen from around 2% three years ago to over 4% today. Higher risk-free rates typically compress PE ratios, making CBA’s elevated multiple difficult to rationalise.

Additionally, risk premiums are often tied to earnings quality, often reflected in return on equity (ROE). CBA’s ROE has declined from 20% before the 2008 Global Financial Crisis to around 13% today. Despite this structural decline in earnings quality, CBA’s price-to-book (PB) ratio is at an all-time high, further highlighting a valuation anomaly.

This sentiment-driven PE expansion mirrors historical bubbles, such as the late 1990s Dot-com bubble or the 2021 COVID-driven market surge. These bubbles typically last 1-2 years before fundamentals reassert themselves, often leading to sharp corrections. CBA’s bubble-like rally is unusually prolonged, raising concerns about whether broader market dynamics are distorting valuations and signaling a broken equity market.

Passive vs. Active Debate

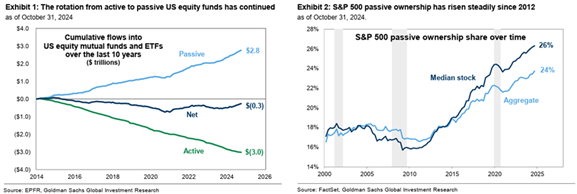

The explosive growth of passive investing is often cited as a potential driver of market distortions. Over the past decade, U.S. passive funds have attracted approximately $3 trillion in assets, at the expense of active managers. Passive ownership of U.S. equities has grown from the high teens to roughly a quarter of total stock holdings. In Australia, similar trends are evident, with passive strategies gaining traction.

Critics argue that passive fund flows inflate valuations of heavily weighted index stocks like CBA. However, a Bloomberg study found no consistent correlation between higher passive ownership and elevated valuations, as stocks in the top decile of passive ownership are not systematically more expensive than those with lower passive ownership.

Valuation Metrics by Level of Passive Ownership

This makes sense as passive funds limit their direct impact on intraday price movements by typically trading at or near market close to minimize performance tracking error and optimize execution during high volume periods.

While passive investing may not directly drive prices, it reduces the pool of shares available of active trading. In the U.S., active managers now account for a small fraction of trading volume compared to two decades ago.

The Composition of Trading has Changed

Despite the smaller share of total trading volume, active managers remain the marginal price-setters, responding to new information and changes in fundamentals. However, a diminished presence weakens the market’s ability to incorporate diverse judgments, which historically kept the market more efficient. This reduction in diversity increases herding behaviour and price volatility, particularly when expectations change rapidly.

In Australia, this dynamic is evident during earnings seasons, where stock prices have over time exhibited greater turbulence in response to new information.

With fewer active managers to counterbalance market reactions, stock prices become more prone to self-reinforcing trends rather than self-correcting mechanisms that align with fundamentals. This dynamic results in more persistent mispricings, exemplified with overvalued stocks like CBA contrasting with undervalued ones such as Treasury Wine Estates (TWE).

Recently, TWE has reported weaker than expected profit updates, which has triggered a significant sell-off in its shares. However, the sell-off looks appears excessive, as its valuation seem disproportionately low comparted to its business quality, as indicated by its ROE.

The lack of sufficient diversity among active managers, who typically bring varied perspectives and investment strategies to identify and correct such mispricings, may delay the market’s ability to restore TWE’s valuation to a level consistent with its fundamentals.

Concentrated Benchmark Amplify the Issue

In a concentrated benchmark dominated by stocks like CBA (10% index weight), active managers face greater hurdles in outperforming. Underweighting a rallying heavyweight like CBA incurs a substantial penalty due to its outsized influence on the benchmark, which may not be offset by being overweight numerous but smaller, outperforming stocks. Skilled active managers who correctly underweight an overvalued stock like CBA may experience short term underperformance and client outflows if its rally persists, even if their long-term view is ultimately validated.

Meanwhile, passive funds and superannuation funds, who are gaining significant market share from active managers become natural buyers of CBA because they prioritise benchmark alignment. This sustained buying further reduces the pool of shares available for active trading, limiting the ability of active managers to correct mispricings. As a result, this dynamic can prolong valuation anomalies, allowing CBA’s overvaluation to persist longer than historical norms.

Conclusion

CBA’s valuation bubble, propelled by an unprecedented PE multiple expansion despite modest earnings growth and declining return on equity, reveals a stark disconnect between market sentiment and fundamentals. The surge in passive investing, while not directly inflating prices, has eroded active management’s influence, diminishing the diversity of perspectives essential for correcting mispricings. This shift fuels herding behaviour, amplifies market volatility and allows valuation anomalies to persist beyond historical norms.

In a concentrated benchmark dominated by stocks like CBA, these dynamics intensify, creating self-reinforcing feedback loops that pose significant challenges for active managers. In an environment of persistent overvaluation or undervaluation, traditional long-term buy-and-hold active strategies may fall short, risking outflows to passive funds. To thrive in this volatile market, active managers must adapt by timing the purchase or sale of mispriced assets, particularly during periods of heightened market turbulence.

Comments